How to Use Personal Capital to Plan Your Long-Term Travels Financially

THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE READ OUR DISCLOSURE FOR MORE INFO.

Last Updated on October 9, 2021 by Amy

(This post is written towards cruisers, but these ideas also apply to long-term travel or early retirement. If you aren’t cruising, you wouldn’t have the lump sum of the purchase or sale of your boat to factor in!)

Cruising finances are one of the biggest topics in the forums, and is often brought up in comments on our blog. Personal Capital has Retirement Planner, a great tool to help you figure out how much money you need in order to go cruising and still make it to the end of your life with financial stability.

- Disclaimer

- Setting Up Personal Capital

- Benefits

- Pitfalls

- Cruising Finance Examples

- Assumptions

- Scenario 1 – Permanent Retirement at 50 & a 6-Year Cruise

- Scenario 2 – Sabbatical at 37 & a 6-Year Cruise

- Additional Scenarios

- How to Interpret Your Results

- Advice from the Experts

Disclaimer

All of the numbers I am using for examples are reasonable numbers. They do not reflect our personal numbers, nor do they reflect extreme situations (like single-paycheck living, minimalism, or the top 1%). Make no mistake – cruising, especially like we do, is a luxury lifestyle.

I’m not a financial expert, I’m just a firm believer in the importance of personal finance education and FI (Financial Independence). Personal Capital is one of my favorite tools to use. This blog is not intended to open up a discussion on complex financial topics (such as bear and bull markets, current policies affecting the global financial market, or stock picks) or even simple topics (like how to save more money or start up a side hustle).

None of the numbers displayed here are from our actual finances. Numbers have also been removed from some graphics to protect our privacy.

You can sign up for Personal Capital, which is free, and get each of us $20. Just click on the image below:

Table of Contents - Click to Jump

Setting Up Personal Capital

Personal Capital is easy to set up, but you do have to remember to add in all your accounts. Fortunately for us, we just have two credit cards, one bank, and two retirement account logins, so it’s not too complicated.

Benefits

Personal Capital is completely free.

The graphics are amazing. Forget using a clunky Excel spreadsheet; Personal Capital takes all the information you give it and automatically creates helpful graphics to help you better understand your finances. For example, this graphic on asset allocation:

Or the dashboard:

Free advice. In addition to the Retirement Planner I’m going to discuss in detail below, Personal Capital has an Investment Checkup tool. When I run the check up I get this simple statement: “Based on your profile, the projected growth rate of your portfolio is appropriate and your asset allocation uses risk efficiently. Adding Bonds would help increase diversification”. There’s other stuff too – charts and more details, but the gist of it is that Personal Capital gives you an actionable item to do to improve your investments quickly.

Pitfalls

Cash tracking is non-existent. Unlike Mint, any ATM withdrawal is lumped into ATM/Cash and can not be divided out into separate categories. For this reason, I still use Mint for budgeting and tracking of expenses. If I was living land-based in the states and barely using cash, I’d use Personal Capital 100%.

Personal Capital representatives are very persistent. You will get calls and emails from Personal Capital offering further free advice and trying to get you to sign up for their consulting. After a while, they get the hint.

Cruising Finance Examples

I’ve pieced together a couple examples so you can see how Personal Capital would work in a few scenarios.

Assumptions

For simplicity, I’ve made two example retirement planners with a base of the same assumptions:

- Current age is 33 years old

- Withdrawal tax rate of 20% (suggested by PC)

- Inflation rate of 4% (suggested by PC)

- Annual return of 8.5% (suggested by PC)

- Annual standard deviation of return of 12.9% (suggested by PC)

- Life expectancy of 92

- Buying a boat at $200,000 **

- Selling the boat at $150,000

- Social Security income starting at 67 for both persons

- Retirement spending of $35,000 a year (this includes boat expenses during cruising and rent after cruising)**

**I pulled these numbers from Beth Leonard’s The Voyager’s Handbook. $35,000 is between Moderation’s spending at $20,000 a year and Highlife’s spending of $60,000 a year. Moderation spent $145,000 on a used boat and $55,000 refitting.

For savings, if you have all your accounts synced with Personal Capital, the savings factor will automatically be filled in with the value of your savings from your dashboard. You can edit this factor, but if you keep it linked to your dashboard, your Retirement Planner will update itself as time progresses.

Scenario 1

Permanent Retirement at 50 & a 6-Year Cruise

In this scenario, at age 33 you’ve bought a house and are starting to save. The savings amount is $40,000 and the savings rate per year is $15,000. The house is sold at age 50, the boat is bought at age 50, and then the boat is sold after a 6-year cruise. Personal Capital gives this scenario a 71% chance at supporting the goals.

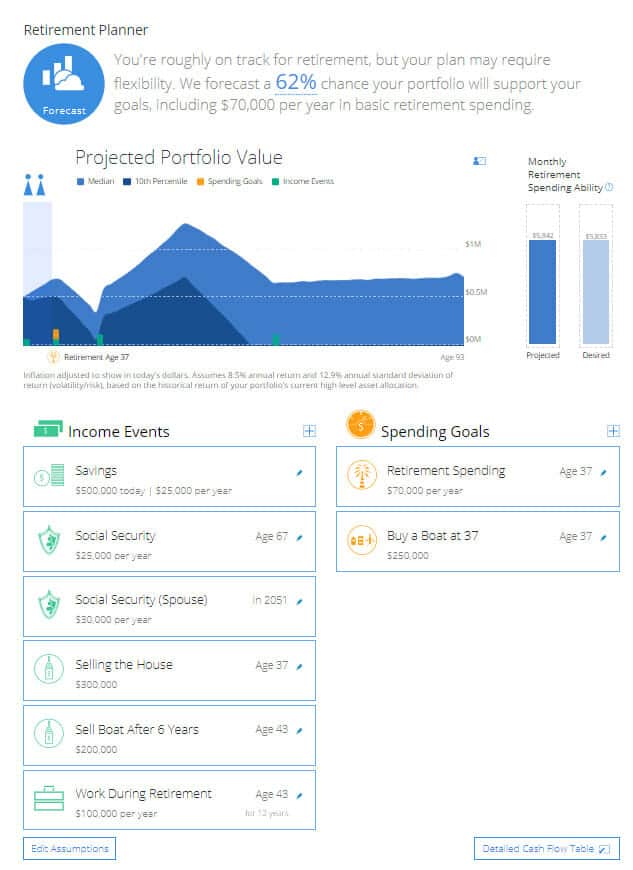

Scenario 2

Sabbatical at 37 & a 6-Year Cruise

This scenario is a bit closer to what we planned when we departed on Starry Horizons in that we had savings, and continued to build those savings up while planning to stop work for 6 years and cruise before coming back to work. In this scenario, there’s no house, instead a much higher savings ($300,000) and savings rate ($30,000). The boat is bought at 37. At the end of cruising, age 43, the boat is sold and the cruisers would go back to work for 12 years (labeled as “Work During Retirement”) before permanently retiring at age 55. Personal Capital gives this scenario a 48% chance at supporting the goals. Obviously this is why you don’t see many young cruisers out – saving the money to buy a boat after just a few years i the workforce is tough work!

Additional Scenarios

Another great thing about the Retirement Planner is that you can run, save, and compare multiple scenarios. For example, here’s a new scenario (Scenario 3) based on Scenario 1, but instead of 6 years, adjust the factors so you cruise for 10 years (sell the boat later and start work later). Now you have a 17% of success. Alternatively, Scenario 4 is identical to Scenario 2, but you decrease your expenses to $20K a year instead of $35K. Now, your success rate is 83%.

How to Interpret Your Results

In scenarios 1 and 2 above, you will notice in the screenshot that the success percentages (71% and 48%) have a link to them. Personal Capital provides this information to help you interpret these results:

“A result between 50% and 80% suggests you are on track, but it is important to understand and acknowledge that the portfolio does deplete in a meaningful amount of the projected scenarios. Results in this range highlight the need for staying disciplined about saving/spending plans and investing efficiently. The ability to be flexible means the odds of a truly bad scenario are even lower than the headline number suggests.”

You have to decide what percentage of success you are comfortable with, and take into consideration how likely it is that you will be able to stick to your savings and spending goals.

I think it’s really beneficial to use this as a tool to motivate yourself. Playing with the numbers can give you a better idea of your finances and the excitement to say something like “if I save X more dollars a year, my % of success increases by Y!”.

Advice from the Experts

There are tons of amazing financial bloggers out there who can provide you with an education into various topics, and are far more experienced than I am:

Where We Be – 10 years after retiring at age 43, Robin and Robert share their net worth.

Mr Money Mustache – the 4% Safe Withdrawl Rate and what that means for retirement.

Go Curry Cracker – a family of 3 that retired in their 30s to travel the world.

No, go plan your adventure!

Want to know more about how much it costs to go cruising? Check out our Cruising Costs blog post.

{kind=link}

Did you looking into using a fiduciary rather than personal capital ?

I think I answered your question via email, but we do not use Personal Capital for investing advice, jus for the free tools. 🙂

How much do you all spend monthly on SH, including things like boat, medical insurance? Thanks!

Hi Stephen! You can check out our blog posts on the costs of cruising: https://outchasingstars.com/cruising-budget-first-year-new-catamaran/

Interesting!

Thanks Mom!